公司

付款需要三周才能结清。隐性费用使发票价值增加 30%。供应商要求在发货前预付 60% 的预付款。欢迎来到非洲的跨境贸易,那里的 “全球商务” 经常在支付阶段死亡。

在当今不必要的复杂国际贸易世界中,信任就是货币。但是对于非洲进口商及其海外供应商来说,由于货币波动和系统性支付壁垒导致的 “信任差距” 日益扩大,这种信任越来越紧张。出现的是一场高风险的游戏,企业必须规避巨大的风险,才能保持货物的跨境流动。

这些数字描绘了非洲贸易融资危机的严峻画面。许多非洲市场的银行仅为商品贸易的25%融资,远低于发达经济体60-80%的融资利率, 根据国际金融公司最近对西非的研究。这种融资短缺具有连带效应:在全球范围内,所有中小企业贸易融资申请中有一半被拒绝,使企业争先恐后地寻找替代方案。

未满足的需求令人震惊。据估计,非洲每年面临的贸易融资缺口为 100-120 亿美元,中小企业——占非洲企业的80-90%——在这场短缺中首当其冲。这些公司通常无法获得信用证或银行担保等传统工具,迫使他们做出不稳定的付款安排。

.jpg)

这种融资缺口在买家和卖家之间的风险分配中造成了危险的失衡。

由于银行融资受到严重限制,非洲进口商面临着不可能的选择。许多人必须完全预先支付进口费用,或者争先恐后地在配给市场上购买稀缺的外汇。例如, 在尼日利亚, 几乎所有的进口外汇都是配给的,几乎所有表格M上都出现 “对外汇无效”,这迫使企业寻求其他资金来源。

尼日利亚中央银行 历史上排除了 43 个产品类别——从大米和水泥到纺织品和包装食品——来自官方外汇准入。尽管2023年取消了对43种商品的限制,但排斥的遗留问题继续将进口商推向昂贵的平行市场和非传统的支付渠道。

这种模式并不是尼日利亚独有的。东非和南部非洲的进口制度通常将整个行业(纺织、家具、钢铁、塑料、农业)标记为没有资格获得官方外汇支持。结果是,正是在企业最需要的时候,系统地将它们排除在正规银行渠道之外。

类似的挑战困扰着整个非洲湾地区的进口商,造成了整个非洲大陆的危机,合法企业被迫进入非正规市场以求生存。

另一方面,由于贸易融资的高拒绝率,国际供应商越来越多地要求在运输货物之前进行有保障的付款。但是,缺乏银行信贷的非洲买家无法提供这些保证,从而造成了扼杀贸易的僵局。

作为 世贸组织笔记,“发展中国家的中小企业在获得贸易融资方面面临最大的挑战”,非洲的短缺约占其市场总需求的三分之一。

即使有传统的贸易融资工具,它们的溢价也是许多非洲企业负担不起的。

非洲市场的信用证通常每笔交易的成本为2-4%,这是一个数量级 高于 0.25-0.5% 的税率 在发达经济体中很常见。这些费用侵蚀了本已微薄的利润率,并将规模较小的参与者推向非正式渠道,进一步分散了市场。

面对这些限制,企业已经制定了变通办法,但代价很高:

这些替代方案的成本很高。截至 2023 年, 撒哈拉以南非洲的汇款费用平均为8.5%,据报道,只有尼日利亚 外汇套利损失了170亿美元 在前一年。结果是,分散的外汇准入和付款延迟系统地破坏了交易效率。

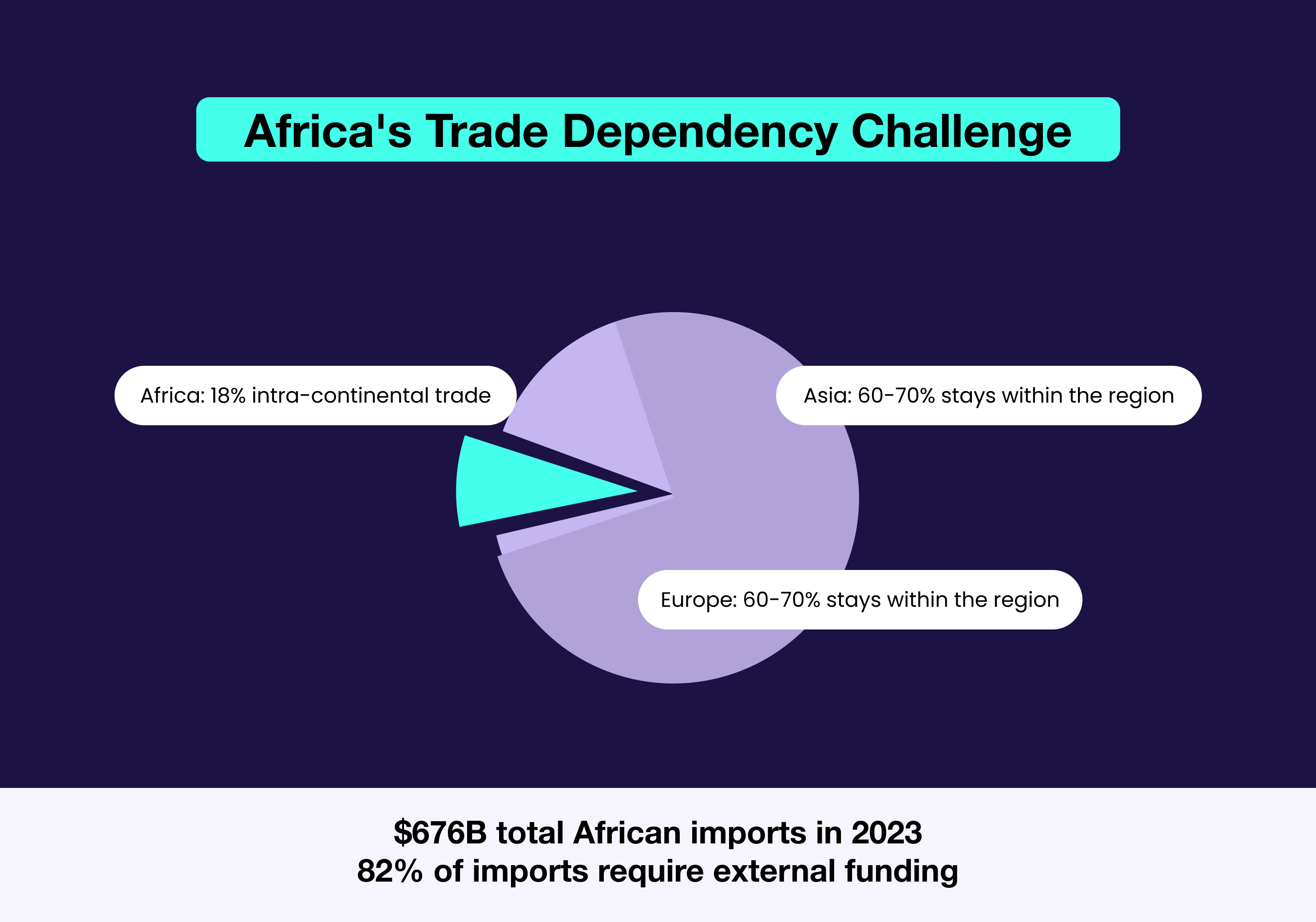

鉴于非洲的进口结构,贸易融资危机尤其严重。只有 约占非洲进口的18% 来自非洲大陆境内,相比之下,亚洲或欧洲境内的贸易中,这一比例为60-70%。这种对外部供应商的严重依赖加剧了付款困难的影响。

2023年,非洲的商品进口总额约为6,760亿美元,但银行只能提供所需贸易融资的一小部分。尽管外汇改革有所改善,但许多公司的融资需求仍不到40%通过官方渠道得到满足。

在 Cedar Money,我们每天都在目睹这些挑战。通过与客户的交谈,我们意识到,除了外汇准入(或缺乏)之外,企业在建立信任方面还面临着非常真实、非常令人沮丧的问题。当银行无法及时签发信用证时,国际出口商越来越多地寻求我们的保证。

这些不仅仅是运营上的不便;它们代表着生存挑战。外汇延迟意味着合同延期,供应商关系受到侵蚀,以及整个供应链的摩擦加剧。累积效应破坏了非洲融入全球贸易网络的进程。

非洲企业面临的基本问题显而易见:在可信、负担得起的外汇准入仍然稀缺的体系中,商业如何继续增长?

我们认为,答案在于通过新的流动性网络和技术解决方案重新构想跨境支付。当企业能够可靠地向供应商付款并且供应商信任付款确定性时,贸易流量自然会增加。研究表明,每1美元的贸易融资可以支持数十美元的实际贸易量。

解决方案不仅仅是政策改革或汇率调整;它需要建设基础设施,使外汇准入更快、更透明,而且对业务更友好。只有解决基本信任差距,非洲企业才能充分参与全球商业,释放非洲大陆的巨大经济潜力。

当前的系统迫使企业进入生存模式。未来需要使他们能够蓬勃发展的工具。

Cedar Money正在建设基础设施,使非洲企业及其全球合作伙伴能够实现可靠、透明的跨境支付。

无论您是为外汇准入而苦苦挣扎的进口商,还是寻求付款确定性的出口商,我们都将帮助您摆脱传统银行业务的限制。

立即开始使用 Cedar Money 并加入已经在体验更快、更实惠的国际支付的企业。

对Cedar Money如何支持您的特定交易需求有疑问吗? 联系我们的团队 进行咨询。